How to Integrate Crypto Payments into Your Business: A Practical Guide

Adding a crypto payment gateway to your business can open new doors. It lets you accept crypto payments from customers worldwide, bringing faster transactions, lower fees, and no chargebacks. But it’s not as simple as flipping a switch. To truly make crypto work for your business, there’s a list of things you need to get right.

Adding a crypto payment gateway to your business can open new doors. It lets you accept crypto payments from customers worldwide, bringing faster transactions, lower fees, and no chargebacks. But it’s not as simple as flipping a switch. To truly make crypto work for your business, there’s a list of things you need to get right.

Set Up a Digital Wallet

A wallet is where digital assets are stored. For daily operations, software wallets can be enough. But for larger amounts, businesses usually choose hardware wallets for added security.

Choose and Integrate a Payment Solution

You'll need a payment gateway that supports digital currencies. This might be a plugin for your e-commerce platform or a custom API integration. The goal is to make payment easy for customers and seamless for your team.

Handle Pricing and Exchange Rates

Decide how to display prices-directly in digital currency or by converting from your local currency at the moment of purchase. Make sure exchange rates are transparent for your customers.

Manage Volatility

Digital currencies are known for price swings. Have a strategy for dealing with this, such as converting to stablecoins or fiat currency immediately after payment.

Monitor Transaction Fees

Network fees can change depending on demand. Regularly review these costs to ensure they remain acceptable for your business.

Stay Compliant

Digital payments are subject to different rules in different regions. Make sure you understand your obligations around KYC (Know Your Customer), AML (Anti-Money Laundering), and other regulatory requirements.

Educate Your Team

Everyone involved should know how the system works-especially your customer service team, who may need to help customers with payment questions.

Communicate with Customers

Let your customers know that you now accept digital payments. Add clear messaging across your website, marketing materials, and checkout flow.

Test Before Launching

Run test payments to ensure the process is smooth from start to finish. This helps catch any issues before customers experience them.

Strengthen Security

Security is a top priority. Use strong authentication, multi-signature wallets, and cold storage for long-term holdings. Keep your security protocols updated.

Set Up Accounting Processes

Track every transaction carefully. Many tax authorities require detailed reporting of digital currency transactions, and having a solid system in place is essential.

Prepare Customer Support

Expect questions and occasional payment issues. Make it easy for customers to contact you and resolve problems quickly.

Stay Informed

The digital payments landscape evolves rapidly. Keep an eye on regulatory changes, new technologies, and market trends to stay ahead.

Get Tax Advice

Digital currency can create tax liabilities. Consult a tax advisor who understands how digital payments are handled in your jurisdiction.

Review and Optimize

Regularly review how digital payments are working for your business. Gather customer feedback and monitor performance to make improvements as needed.

How INXY Payments Supports These Steps

At INXY Payments, we've built our platform to address all these challenges in one place. Our service is designed for businesses that want to add digital currency payments with minimal friction and maximum compliance. Here's how we help:

Auto-conversion: Incoming payments can be automatically converted to stablecoins or fiat currency to minimize volatility.

Full Compliance: Our platform is fully compliant with MiCA and other EU regulations, with built-in tools for KYC and AML checks.

Seamless Integration: Whether you use the API or our dashboard, setup is simple and fast.

No Wallet Management: You don't need to create and maintain wallets on different blockchains or hold extra coins to pay network fees-we handle that for you.

Custom Reports: We provide detailed, customized reports to simplify your accounting and tax filing.

Security First: Advanced security features protect your funds at every step.

Global Reach: We support payments worldwide and work across multiple industries.

Expert Support: Our team offers personalized onboarding and ongoing assistance, including tax consultations and compliance help.

Always Up-to-Date: We stay on top of blockchain updates and new infrastructure developments, so you don't have to worry about keeping up with tech changes.

Whether you want to accept bitcoin payments, send mass payouts in crypto, or add a seamless crypto billing option to your service, we've got you covered.

Stablecoin Payments: Why Businesses Switch in 2025

Discover why businesses worldwide are switching to stablecoin payments in 2025. Learn how stablecoins work, their benefits over traditional payments, real case studies, global regulations, and what the future of digital payments looks like

Stablecoin payments are a way to use digital currencies that are pegged to stable assets, like the US dollar. This means their value doesn't swing wildly like other cryptocurrencies. Imagine you're doing business online, and you want to avoid the ups and downs of Bitcoin's value. Stablecoins, like USDC, DAI and USDT, come in handy here. They offer the benefits of crypto without the same level of risk.

These payments work through a crypto payment gateway, which acts like a bridge. It lets businesses accept stablecoins and convert them into local currency if needed. This is helpful for companies that want to tap into the crypto market without holding onto volatile assets.

Think of stablecoin payments as a digital version of cash that you can use globally, without worrying about big price changes. They're fast, often cheaper than traditional methods, and open up new markets for businesses. This makes them a popular choice for companies looking to innovate in 2025. Stablecoins also help people in emerging markets who have no access to traditional banking. Many do not have a bank account, but almost everyone has a mobile phone. Stablecoins give these users a safe and simple way to pay online.

The Rise of Digital Transactions

Digital transactions have become increasingly popular as we move further into the 21st century. People use digital payments to buy things online, pay bills, and even send money to friends. This shift has been driven by the need for faster, more convenient ways to pay.

One example is mobile wallets, which let you store your credit or debit card information on your phone. This makes it easy to pay with just a tap. Businesses are also seeing the benefits. They can reach more customers who prefer digital payments, and they can process transactions more quickly.

Cryptocurrencies like Bitcoin and stablecoins like USDC and USDT offer new ways to pay digitally. These currencies are secure, and they don't rely on traditional banks. This can lower costs and increase access to financial services.

The growth of digital transactions is also supported by better technology. Faster internet speeds and improved security measures make it easier and safer for everyone to use digital payments. As more people and businesses adopt these methods, digital transactions are set to become the norm.

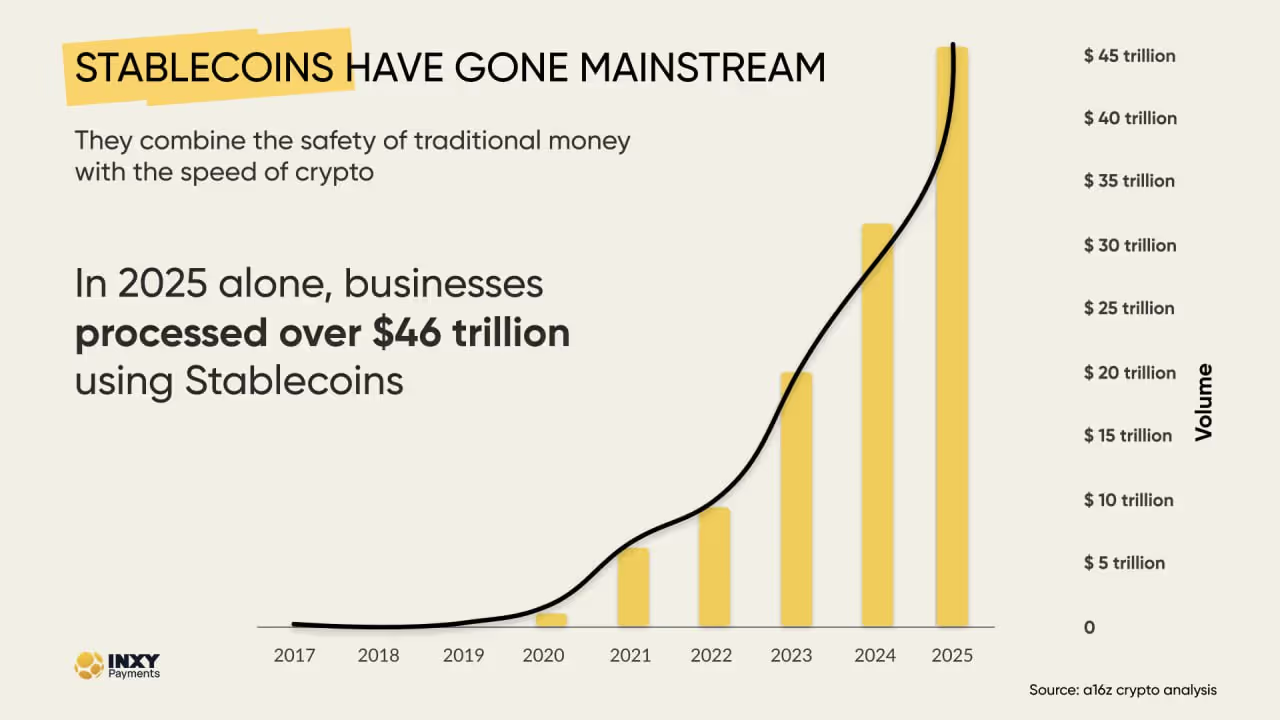

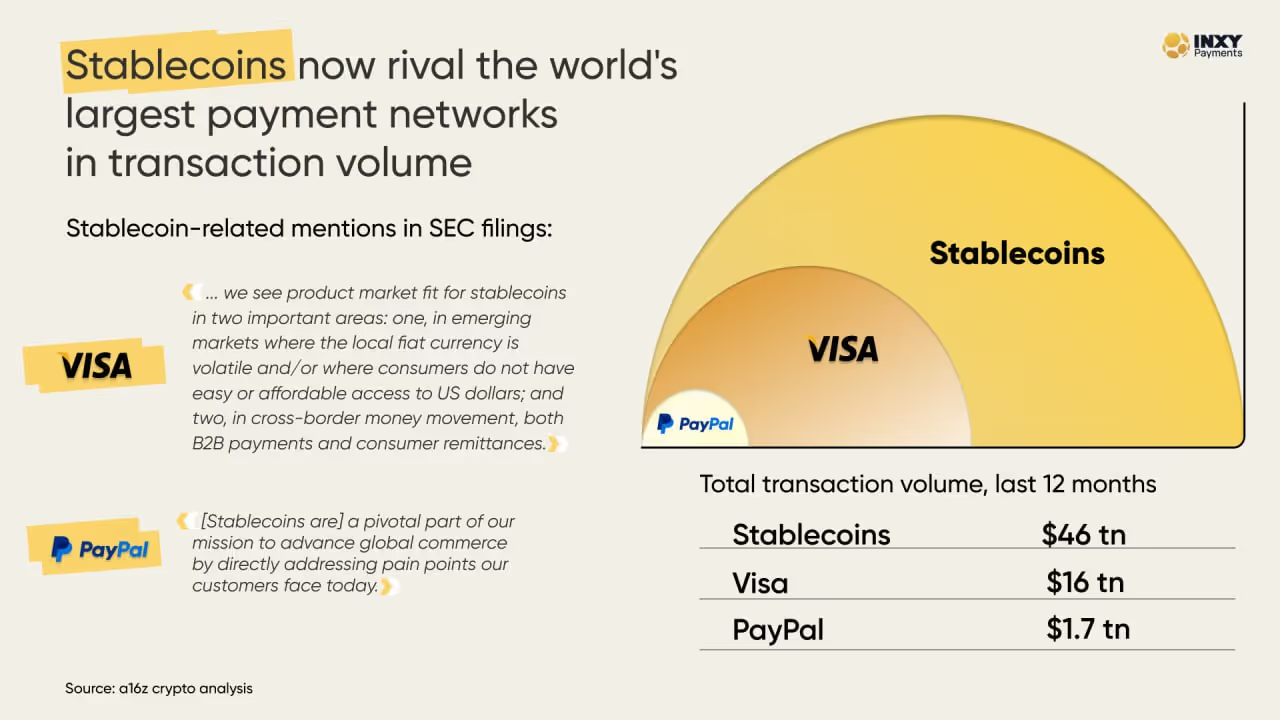

Today, more than 824 million people worldwide own cryptocurrency.

Stablecoins alone processed over $46 trillion last year — more than Visa and PayPal combined.

This shows that digital payments are not a niche trend. They are becoming the main way money moves online.

Benefits for Businesses

Stablecoin payments offer several advantages for businesses. They're less volatile than other cryptocurrencies like Bitcoin. Imagine you're a business owner. You want to know the value of your money won't change drastically overnight. Stablecoins, backed by assets like the US dollar, provide that peace of mind.

Transaction fees with stablecoins can be lower than traditional banking systems. This means businesses save money, especially on international transactions. For example, sending money across borders usually involves hefty fees. With stablecoins, these costs can be minimized.

Another perk is the speed. Traditional bank transfers can take days. Stablecoin transactions, on the other hand, can be processed in minutes. This speed is crucial for businesses that need quick access to funds. Plus, the use of stablecoins can open doors to new markets, reaching customers who prefer using digital currencies.

also let businesses reach new markets. Many people in emerging regions cannot use cards or access banks, but they can use digital wallets and stablecoins on their phones. This opens the door to millions of new customers who were previously locked out of traditional online payments.

Challenges of Traditional Payment Methods

When we talk about traditional payment methods, we're often referring to cash, credit cards, and bank transfers. While these methods have been the backbone of commerce for years, they come with their own set of challenges. Let's explore these issues to understand why businesses are looking at alternatives like stablecoin payments.

Traditional payments are slow and costly. Bank transfers and card payments can take days to settle, especially across borders. Fees are also high — from card fees to bank transfer fees to currency conversion charges — cutting into margins and slowing business growth.

Security is another concern. Credit card fraud and data breaches are not uncommon. When customers hand over their card details, there's always a risk of that information being misused. This situation not only affects the customers but can also damage the business's reputation. A single security breach might lead to a loss of customer trust, which takes a long time to rebuild.

Limited access is an issue too. Not everyone has access to credit cards or bank accounts. Some customers might prefer alternative payment methods like digital wallets or cryptocurrencies. Businesses that only accept traditional payments could miss out on potential sales from these customers. It's like having a store but keeping the door locked for some shoppers.

Traditional payments also lack transparency. It's often hard for both businesses and customers to track where the money is at any given moment. For example, if a payment is delayed, it can be challenging to pinpoint the reason or the stage at which it's stuck. This lack of visibility can cause frustration and distrust among customers.

Lastly, there's the issue of adaptability. As technology evolves, businesses need payment systems that can keep up with the changes. Traditional payment methods are often slow to adapt to new needs and innovations. For instance, they might struggle to integrate with new e-commerce platforms or to support emerging payment trends.

These challenges make it clear why businesses are exploring other options. Stablecoin payments offer solutions to some of these issues, providing a faster, more secure, and cost-effective alternative. As businesses continue to grow and change, finding flexible payment solutions becomes even more critical.

Case Studies: Companies Making the Switch

Let's dive into some real-world examples of businesses that have embraced stablecoin payments. Each company has its unique reasons, and their experiences offer valuable insights for others considering this path.

One notable case is a well-known online retailer. This company decided to accept USDC, DAI and USDT as part of their payment options. The primary motivation was the global reach of crypto. Customers from different countries found it easier to pay in stablecoins without worrying about currency conversion issues. It also allowed the retailer to reduce transaction fees, which were a burden when using traditional payment gateways.

Another interesting example is a tech startup focused on software development. They started accepting stablecoin payments for their services. The team found that using a crypto payment gateway streamlined their operations. It provided faster transaction times and reduced paperwork. The transparency of blockchain technology also appealed to their tech-savvy customers, who appreciated the added layer of security.

A third case involves a popular restaurant chain. The chain began to accept stablecoin payments during the pandemic. Traditional cash payments were less desirable due to health concerns. By adopting stablecoins, they not only offered a contactless payment solution but also attracted a younger clientele. Many of these customers were already familiar with crypto and eager to use it in everyday transactions.

Then there's a logistics company that made the switch. This company operates internationally, and stablecoins helped them manage cross-border payments more efficiently. The predictability of stablecoin values, unlike volatile cryptocurrencies, made financial planning easier. They could handle transactions with partners and vendors with greater confidence in cost predictability.

Lastly, a freelance platform adopted stablecoin payments to simplify payouts to freelancers around the globe. Freelancers appreciated receiving payments in USDC or USDT for their stability and ease of conversion to local currencies. This shift also solved issues related to delayed payments through traditional banking systems.

These examples illustrate the diverse motivations behind the switch to stablecoin payments. From reducing costs to improving speed and security, businesses find multiple benefits in adopting this modern approach. Each company's journey showcases how stablecoin payments can address specific challenges and open up new opportunities.

These stories reflect a broader trend. In 2024 and 2025, stablecoins became one of the fastest-growing payment methods worldwide, especially for online services and global businesses.

Regulatory Landscape in 2025

Stablecoin payments have been gaining traction, and 2025 is shaping up to be a pivotal year for their regulation. Governments around the world are crafting policies to manage these digital currencies. This is crucial as stablecoins like USDC and USDT become more popular in the business world.

One major development is the introduction of global standards. International bodies are working to create a unified framework for stablecoin regulation. This helps ensure that businesses using stablecoins can operate smoothly across borders. Without such standards, companies might face different rules in each country, making international trade complex.

Local governments are also busy. Each country is trying to balance innovation with security. They want to encourage the use of stablecoins while making sure that financial systems remain safe. For example, some countries are adopting stricter compliance measures. This means businesses need to ensure all transactions are transparent and traceable.

In the European Union, new laws are being drafted. These laws aim to protect consumers and prevent illegal activities. They require that stablecoin providers hold sufficient reserves. This ensures that the value of the stablecoins remains stable and reliable.

Meanwhile, in the United States, regulators are focusing on oversight. They want to ensure that stablecoin issuers are transparent about their operations. This includes regular audits and public disclosures. Such measures help build trust among users and businesses.

Asia is also seeing changes. Countries like Japan and Singapore are leading in creating crypto-friendly regulations. They are developing policies that encourage innovation while ensuring that user rights are protected.

These regulatory changes are significant for businesses. Companies need to stay informed and adapt to these new rules. Understanding the regulatory landscape is key to leveraging stablecoin payments effectively. As 2025 unfolds, businesses will need to navigate this evolving landscape carefully.

The Future of Payments: What’s Next?

Stablecoin payments are gaining popularity, and it's not hard to see why. They bring a fresh wave of possibilities to the table. Businesses are starting to notice how stablecoins can change the payment landscape. Let's explore what the future might hold.

One big reason stablecoins are appealing is their stability. Unlike other cryptocurrencies, stablecoins are tied to real-world assets like the US dollar. This means they don't bounce around in value as much. For businesses, this stability is a huge plus. They can accept payments without worrying about losing money due to market fluctuations.

Stablecoins also make international payments easier. In the past, sending money across borders was slow and costly. With stablecoins, transactions can be completed quickly and with lower fees. This is great news for companies working with international clients or suppliers. It allows them to save both time and money.

Security is another reason businesses are interested in stablecoins. Traditional payment systems can be vulnerable to fraud and hacking. Stablecoins offer a more secure option as transactions are recorded on a blockchain. This technology makes it difficult for unauthorized changes to occur.

Looking ahead, we might see stablecoins being used in more everyday transactions. Imagine buying a coffee or paying rent with stablecoins. As more businesses and consumers become comfortable with the technology, this could become a reality.

Stablecoins may also impact how we save and invest money. People are starting to explore options like earning interest on their stablecoin holdings. This could lead to new financial products and services emerging in the market.

In the coming years, regulations will play a crucial role in shaping the stablecoin landscape. Governments and financial institutions will likely establish rules to ensure safe and fair use. These regulations could boost trust and encourage more businesses to adopt stablecoin payments.

The future of payments is changing, and stablecoins are at the forefront. As technology continues to evolve, we can expect even more innovative uses for stablecoins. They have the potential to simplify and enhance the way we handle money.

Supported Stablecoins & Blockchains (2025)

Many stablecoins run on different blockchains. This makes payments fast and affordable anywhere in the world.

Supported stablecoins:

USDT — ERC20, TRC20, BEP20, Polygon

USDC — ERC20, TRC20, BEP20, Polygon

DAI — ERC20, BEP20, Polygon

Other popular coins: BTC · ETH · BNB · LTC · DOGE · TRX · MATIC

Supported blockchains: Bitcoin · Ethereum · Tron · Polygon · Binance Smart Chain · Litecoin · Ton · and others. The mix of currencies and blockchains makes stablecoin payments work for almost anyone, even in places where card payments fail.

FAQ

What are stablecoin payments and how do they work?

Stablecoin payments involve using digital currencies designed to minimize price volatility by pegging their value to a stable asset, like a fiat currency or commodity. They work like any other digital payment method but offer the added benefit of price stability, making them more reliable for transactions.

Why are stablecoins becoming popular in digital transactions?

Stablecoins are gaining popularity in digital transactions due to their ability to offer the benefits of cryptocurrencies, such as decentralization and transparency, while avoiding the price volatility associated with traditional cryptocurrencies. This makes them an attractive option for businesses looking for secure and stable payment methods.

What benefits do stablecoin payments offer to businesses?

Stablecoin payments provide several benefits, including lower transaction fees compared to traditional payment methods, faster processing times as transactions are often completed in seconds, and enhanced security due to blockchain technology, which reduces fraud and chargebacks.

What challenges do traditional payment methods face that stablecoins address?

Traditional payment methods often suffer from high transaction fees, lengthy processing times, and issues with cross-border payments. Stablecoins address these challenges by offering reduced fees, instantaneous transactions, and seamless international payments, thus providing a more efficient alternative.

Can you provide examples of businesses that have switched to stablecoin payments?

Many companies across various industries have transitioned to stablecoin payments. For instance, a tech company might use stablecoins to streamline international payroll, while an online retailer could adopt them to reduce transaction costs and improve payment processing speed.

How is the regulatory landscape for stablecoins evolving in 2025?

In 2025, the regulatory landscape for stablecoins is evolving to provide clearer guidelines and protections for businesses and consumers. Governments and financial bodies are working on frameworks to ensure stablecoin security and transparency, influencing business decisions towards stablecoin adoption.

In the European Union, the new MiCA framework brings clear rules for stablecoins and crypto service providers. These rules aim to protect users while supporting innovation. Similar frameworks are emerging in Asia, the U.S., and Latin America.

What does the future hold for stablecoin payments and their impact on the economy?

The future of stablecoin payments looks promising, with potential for widespread adoption as more businesses recognize their benefits. This could lead to significant changes in the payment industry, driving innovation and possibly reshaping economic structures by making transactions more efficient and accessible worldwide.

How to Verify a Merchant Account? Step-by-Step Guide

Navigating the regulatory landscape of 2026 is crucial for any business accepting digital assets. This guide provides a comprehensive, step-by-step walkthrough of the merchant verification process for crypto payment gateways in the European Union. From understanding the Markets in Crypto-Assets (MiCA) regulation to mastering the Know Your Business (KYB) documentation requirements, we detail exactly how to secure a verified, bank-grade account. Whether you are in e-commerce, hosting, or high-risk industries, this unified framework ensures your business is compliant, secure, and ready for the global economy.

5 min read

13.2.2026

The institutionalization of the digital asset economy within the European Union has reached a definitive stage. As the financial sector navigates the complexities of the mid-2020s, regulatory compliance and operational excellence are no longer optional for businesses seeking to leverage blockchain-based financial rails.

For crypto payment gateways based in the EU, such as INXY Payments, the verification workflow represents the first and most critical touchpoint in establishing a secure, bank-grade relationship with professional partners. This report provides an exhaustive analysis of the merchant verification process, grounded in the primary directives of the Markets in Crypto-Assets (MiCA) Regulation and the practical requirements of the Know Your Business (KYB) standards.

The Regulatory Landscape: MiCA, TFR, and DAC8

The "Regulatory Rubicon" has been crossed, shifting the focus of European authorities from drafting policy to aggressive enforcement. Central to this environment is the Markets in Crypto-Assets Regulation (MiCA), which has successfully harmonized the rules for digital assets across all 27 EU member states.

The verification process is now governed by three key frameworks:

MiCA Authorization: Eliminates the "Wild West" era, ensuring only fully authorized providers operate within the EEA.

Transfer of Funds Regulation (TFR): Enforces a "Zero Threshold" policy for the "Travel Rule," requiring detailed data on the originator and beneficiary for every transaction.

DAC8: Mandates strict tax reporting and the collection of Tax Identification Numbers (TINs) to ensure fiscal transparency.

Architecture of the Know Your Business (KYB) Process

Know Your Business (KYB) is the primary defensive mechanism used by fintech gateways. Unlike Know Your Customer (KYC), which focuses on individuals, KYB requires a deeper exploration of corporate hierarchies.

The Verification Objectives:

Legal Existence: Proving the business is a real, registered entity.

Control Disclosure: Identifying the Ultimate Beneficial Owners (UBOs) to prevent the use of shell companies for illicit activities.

Risk Scoring: Evaluating the industry, geography, and transaction profile of the merchant.

The INXY Payments Verification Workflow: A Step-by-Step Guide

The verification process is designed to be rigorous yet streamlined, ensuring all participants meet EU compliance standards. This is a unified process applicable to all merchants, regardless of their industry or integration method.

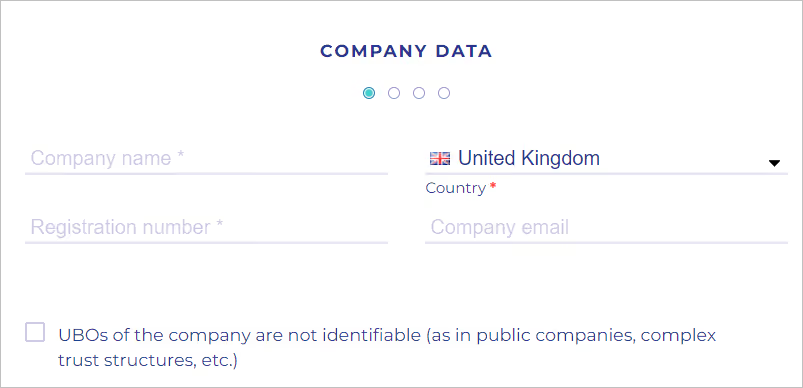

Step 1: Initial Company Data Intake

The process commences with the "Company data form." The merchant must enter fundamental identifying information, including the legal Company Name, official Registration Number, and Country of Registration.

Note: Providing a direct company email is recommended to ensure a clear line of communication with compliance officers.

Step 2: Comprehensive Documentation Upload

Merchants must validate their legal status by uploading a robust evidentiary file. Mandatory documents typically include:

Certificate of Incorporation / Business Registration: Proof that the entity exists in a government registry.

Articles of Association (AOA): Defines the entity's operations and leadership structure.

Operating License: Required only if the merchant operates in a specifically regulated sector (e.g., gambling, forex).

Identifying the natural persons who ultimately control the entity is the cornerstone of EU AML regulations.

The 25% Rule: Merchants must identify any natural person holding more than 25% of ownership shares or voting rights.

Verification: For each UBO, the system requires their full name, date of birth, and contact details. Identity verification can be performed live or via a secure link sent to the stakeholder.

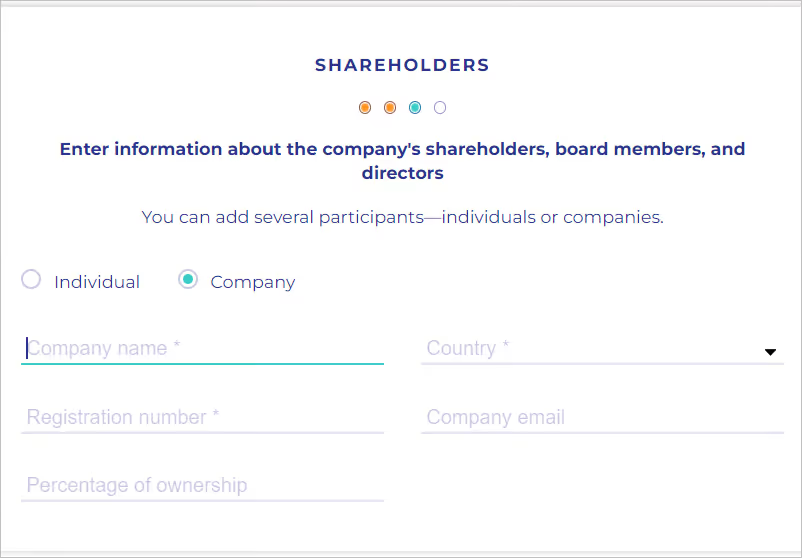

Step 4: Shareholder and Representative Verification

Corporate Shareholders: If a shareholder is another company, the merchant must provide that entity's Articles of Association and trace the ownership chain back to a natural person.

Legal Representative: Data must be provided for the person acting on behalf of the company, ensuring they have the legal authority (e.g., Director status or Power of Attorney) to open financial accounts.

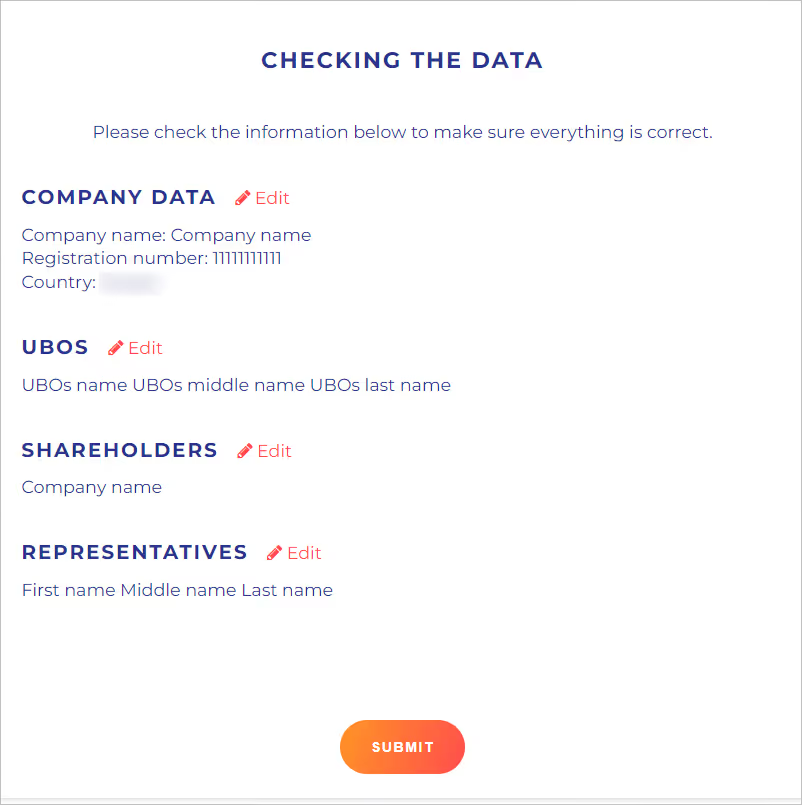

Step 5: Final Validation and Submission

The penultimate step is a thorough review of all provided data. Once confirmed, the application enters the compliance review queue. Thanks to automated systems, merchants can track their status in real-time via their dashboard.

Document Requirements and Authentication Standards

The integrity of the verification process relies entirely on the quality of the documentation. The European fintech environment maintains a high bar for validity.

Mandatory Conditions for Approval:

Language: All documents must be in English. If the original is in another language, a notarized translation is required.

Authentication: Documents must be "official," bearing the necessary stamps, signatures, or qualified electronic seals as per local laws.

Recency: Extracts from commercial registries generally should not be older than 3 months to ensure the data is current.

Common Reasons for Rejection:

Typos: Mismatches between the input form and the uploaded PDF.

Missing Pages: Uploading incomplete Articles of Association.

Low Quality: Blurry scans or photos where text is illegible.

Security and Data Protection (GDPR & DORA)

The sensitive nature of KYB data requires the highest levels of protection.

GDPR Compliance: Data is used solely for client identification and activity justification, adhering to the principle of "Purpose Limitation."

DORA (Digital Operational Resilience Act): Mandates that payment gateways demonstrate resilience against cyber threats. Data is encrypted at rest and in transit, with role-based access ensuring only authorized compliance personnel can view identity files.

Conclusion: Compliance as a Competitive Advantage

Completing the merchant verification process is more than a regulatory hurdle; it is a strategic move that positions a business as a credible player in the global economy. By adhering to this standardized verification workflow, merchants—whether they are hosting providers, e-commerce stores, or digital service agencies—secure a stable, bank-grade foundation for their financial operations.

In the mature crypto economy of 2026, a verified account is the key to unlocking global markets, ensuring seamless settlements, and protecting business capital from regulatory friction.

How to Integrate a Crypto Payment API: A Developer’s Guide for 2026

Integrating crypto payments is no longer just about generating a wallet address—it’s about building a robust, scalable financial pipeline. In this 2026 Developer’s Guide, we strip away the complexity of blockchain interactions and provide a clear roadmap for API integration.

How to Integrate a Crypto Payment API: A Developer’s Guide for 2026

In the fast-moving world of fintech, the question is no longer if a business should accept cryptocurrency, but how seamlessly it can be integrated. As we move through 2026, the European market has reached a point of high maturity. With the full enforcement of MiCA (Markets in Crypto-Assets) regulations, crypto payments have transitioned from a niche experiment to a standardized financial tool for EU-based enterprises.

For developers and product managers, integrating a crypto payment API is now as streamlined as traditional fiat gateways, provided you follow the right architectural patterns.

1. Understanding the 2026 Integration Workflow

Modern crypto integration follows a predictable RESTful pattern. Unlike the early days of manual wallet monitoring, today’s gateways handle the blockchain's complexity, allowing your backend to interact with simple JSON payloads.

The standard lifecycle of a crypto payment includes:

Initialization: Your server requests a unique payment address for a specific order.

Monitoring: The gateway monitors the blockchain (Bitcoin, Ethereum, Tron, etc.) for incoming transactions.

Confirmation: The gateway verifies the transaction depth (number of block confirmations).

Webhook Notification: Your system receives an asynchronous callback to update the order status.

2. Step-by-Step API Integration

Phase A: Environment Setup

Before hitting production, high-quality gateways provide a Sandbox environment. This allows you to simulate successful payments, timeouts, and underpayments without risking real capital. You’ll typically need two headers for every request:

X-API-KEY: Your unique identifier.

X-PAY-SIGNATURE: A HMAC-SHA512 hash to ensure data integrity.

Phase B: Creating the Payment

To start a checkout, your backend sends a POST request to the /invoices or /payments endpoint.

The gateway responds with a destination address and a QR code URL. In 2026, the best UX practice is to offer "Invisible Crypto"—where the user sees a familiar interface, and the gateway handles the real-time conversion behind the scenes.

Phase C: Handling the Webhook

This is the most critical part of the integration. Since blockchain transactions are asynchronous, your server must be ready to receive a POST callback.

Pro Tip: Always verify the webhook signature. Never update an order status based solely on the incoming payload without checking that the request actually originated from your provider.

3. Security and Compliance in the EU

In the 2026 fintech landscape, security isn't just about encryption; it's about regulatory alignment. Within the EU, businesses must ensure their payment partner adheres to Transfer of Funds Regulation (TFR) and AML (Anti-Money Laundering) standards.

When choosing a provider, look for features like:

Auto-Conversion: Instantly swapping volatile assets into stablecoins or EUR to protect your margins.

Audit-Ready Reporting: Financial statements that your accounting team can actually use for VAT and tax filings.

This is where specialized gateways like INXY (inxy.io) excel. Built specifically for the EU market, INXY acts as a regulated bridge. It doesn't just provide an API; it provides a compliant infrastructure that allows Web2 companies to scale into Web3 without the headache of managing private keys or worrying about crypto volatility. By integrating a solution like INXY, businesses can reduce processing fees by up to 70% compared to traditional card networks, while benefiting from instant SEPA settlements.

4. Testing and Optimization

Before going live, run "Chaos Tests" on your integration. What happens if a user sends too little? What if they pay after the 20-minute price-lock window? A robust API should provide clear error codes for these scenarios, allowing your frontend to guide the user toward a resolution—such as a partial refund or a top-up payment.

Conclusion

Integrating a crypto payment API in 2026 is a strategic move that opens your business to a global, tech-savvy audience. By utilizing professional gateways that handle the heavy lifting of compliance and conversion, your team can focus on what matters: the product.

Ready to modernize your payment stack? Would you like me to draft a technical checklist for your dev team to use during the INXY sandbox testing phase?

.avif)